Ask a MoFo: I Have a Company That Was Formed in Another Country, but I Want to Set up My Business for VC Investors (Ideally Having Them Invest in a Delaware Corp.). How Do I Process and Structure Something like That?

The following article is part of our "Ask a MoFo" series, where we address some of the frequently asked questions our MoFo startup team is asked during the course of business. These questions span the entirety of the startup lifecycle – from questions relating to incorporation, to tips for a successful exit. We encourage you to submit questions you would like to see answered as part of this series to ECVCevents@mofo.com.

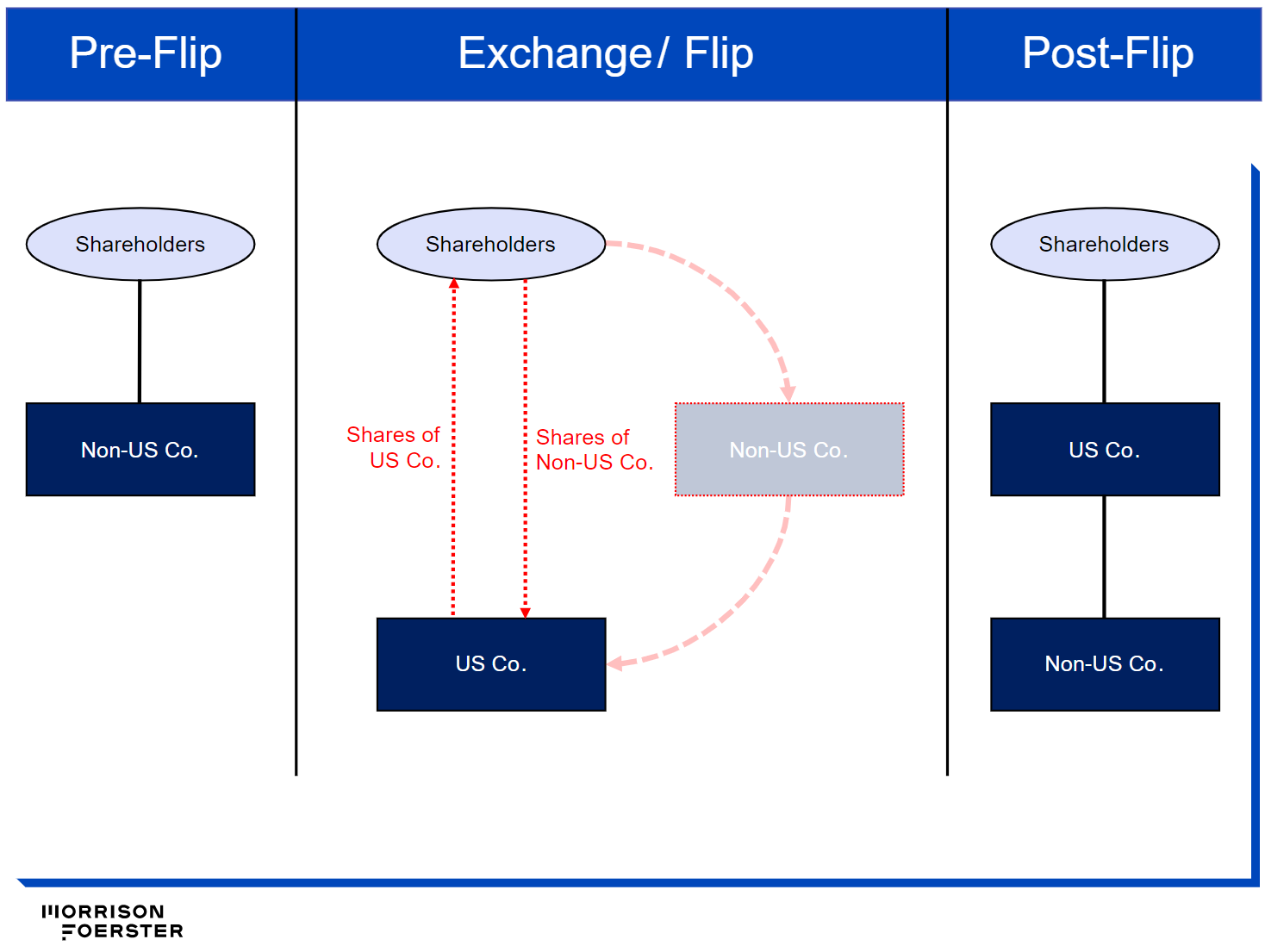

U.S. Company Flip

Emerging companies formed outside the United States may want to redomicile their businesses to the United States to, among other things, enhance their fundraising prospects. U.S. venture capital investors often require non-U.S. companies to flip into Delaware corporations as a condition to investment. Given that custom and preference, non-U.S. startups may choose to redomicile to the United States in advance to well position themselves to receive U.S. venture capital quickly, eliminating potential setbacks or pre-conditions during the investment process itself.

This note focuses on how to efficiently flip from a non-U.S. company to a U.S. company, with a Delaware corporation as the new parent. Why Delaware corporations are the optimal corporate form for startups seeking U.S. venture capital will be the subject of another article.

Steps

An efficient way to flip from a non-U.S. to a U.S. company is to do a share-for-share exchange, where shares of the original non-U.S. company are given up in exchange for shares of a new U.S. company. The steps to do so include:

- The formation of a new Delaware corporation, and

- The exchange of shares of the original non-U.S. company for shares of stock of the new Delaware corporation.

The exchange can be done on a one-for-one (1:1) basis, where each outstanding share of the original non-U.S. company is exchanged for one newly issued share of the new U.S. company, or at some other ratio (e.g., one-for-ten (1:10) or one-for-one-tenth (1:0.1)) to achieve the desired post-exchange capitalization of the U.S. parent company. The same exchange ratio is consistently applied to all shareholders so, regardless of the exchange ratio chosen, the shareholders will own the same percentage of the business both before and after the exchange.

In addition to exchanging all outstanding shares, all convertible, exercisable, or exchangeable equity interests of the company (such as convertible notes, options, or warrants) are exchanged (at the same ratio) as well.

This structure typically requires cooperation from each shareholder and each holder of convertible, exercisable, or exchangeable equity interests, so it is important to consider taking this step early in the company’s life.

After these steps:

- The shareholders will own 100% of the new Delaware corporation, and

- The new Delaware corporation will own 100% of the original non-U.S. company, making it a wholly owned subsidiary.

Tax Considerations

Although the share-for-share exchange is structurally and procedurally efficient, analyzing the potential tax consequences of a share exchange can be complex and must be done on a case-by-case basis because the tax treatment depends on the applicable tax rules in the jurisdictions of the shareholders and the original non-U.S. company. Optimally, a well-structured flip would:

- Be done on a tax-free basis as to both the shareholders and the companies, and

- Carry over and preserve the tax characteristics of the original shares (e.g., cost basis and holding period).

If a share-for-share exchange structured flip would result in an undesirable tax outcome, other transaction structures can be explored.

Importantly, flipping from a non-U.S. to a U.S. parent company is often viewed as an irreversible decision from a U.S. tax perspective. Because of the strict anti-inversion regime under U.S. tax law, if the company later attempts to flip from a U.S. to a non-U.S. parent company, the new non-U.S. parent would generally continue to be subject to U.S. tax as a U.S. company, with limited exceptions and structuring alternatives.

Conclusion

Redomiciling to the United States is a major corporate decision, requiring the time, attention, and alignment of many of the company’s stakeholders. Generally, it is simplest to flip a company to the United States while the company is in a very early stage; it becomes more complex (from a legal, tax, accounting, and practical standpoint) to do so as the business matures. Professional legal, tax, and accounting advice should be sought for any companies looking to flip their jurisdiction of formation to the United States.

Originally posted as a client alert on www.mofo.com.

Receive invites to MoFo startup events and legal updates

ScaleUp

Legal Guidance for Startups